Vertical Divider

|

U.S. Partisan Political Environment Interfering with Trade Dispute Settlements

October 21, 2019 Trade disputes have been an ongoing soap opera since President Trump took office. From steel tariffs to trade skirmishes with China, Japan, Canada, Mexico, South Korea, and the European Union, among others, it's been hard to keep track! But over the past few months, a trend toward settlement of these disputes has emerged. Congress must still act on the new version of NAFTA with Mexico and Canada – USMCA – but as Democrats in the House of Representatives consider impeaching the president, they should also become more interested in showing they're not only interested in all scandal, all the time. Passing some broad bi-partisan legislation and USMCA would be a good start. Look for it to get passed by early 2020, putting our disputes with our two largest export markets behind us. From the perspective of US economic growth, the relationship with China has received way too much attention in the past couple of years. Even before the trade dispute started, US exports to China were a smaller share of our GDP than exports to Japan were before the Japanese economy went into a long-term funk in the early 1990s. If the US could prosper in the 1990s in spite of Japan's problems, the US economy overall should be able to absorb softer demand for our products coming from China, which lags well behind Canada and Mexico as an export market. |

|

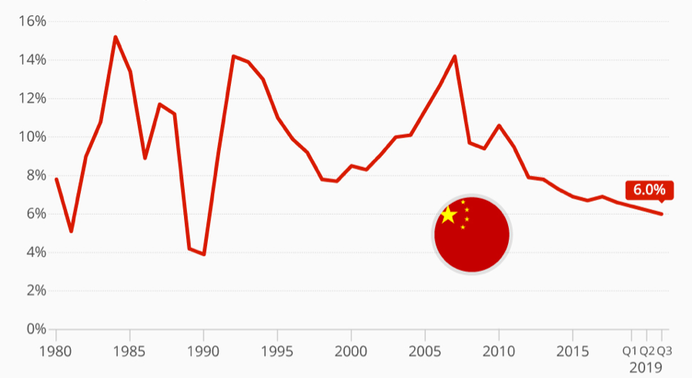

But last week's news indicates a deal is getting close. It may take 4-week to paper it and it’s not the huge deal that comprehensively puts all our trade issues with China to rest; not even close. But it will likely mean no new additional restrictions from now through 2020, and some rolling back of tariffs put in place in the last couple of years. Meanwhile, the US recently concluded a trade deal with Japan. China missed the post-world War II economic bonanza but clearly made up for it starting in the mid 90s. Thirty years of 8-10% GDP growth is unprecedented, so the recent drop back to a strong 6% growth should be no surprise or recognition of an economic trend.

Figure 1 China’s GDP Growth

Figure 1 China’s GDP Growth

Source: China’s National Bureau of Statistics

None of this suggests we are fully out of the woods on trade issues. It’s doubtful China will change its position on intellectual property, and so, a trade dispute with China could re-emerge in 2021 no matter who wins the presidential election next year. In the meantime, tariffs and the threat of other economic sanctions on China were always more damaging to China than the US. But nothing that's happened in the last few years suggests we are entering some sort of Smoot-Hawley-like downward spiral in international trade. US merchandise imports dropped 70% from 1929 to 1932 while exports dropped 69%. That's a downward spiral! US imports didn't reach 1929 levels again until 1946. By contrast, even before the recent trade deals with Mexico, Canada, and Japan have been implemented, US trade with the rest of the world has been rising. In the past twelve months, exports and imports of goods and services combined have been $5.65 trillion, versus $5.63 trillion in calendar 2018, $5.26 trillion in 2017, and $4.93 trillion in 2016. Even without deals, trade could be hitting a record high this year. The US economy has been and will continue to be much more resilient than many think. Trade has increased uncertainty, but was never as big a threat as feared. And, as trade relations improve, stocks will make up lost ground. We were never as worried as the conventional wisdom, and now it will come around. From: First Trust Advisors L. P.