Vertical Divider

Samsung’s Lead in OLED Display Production Drops from 81.7% in Q120 to 51.5% in Q221

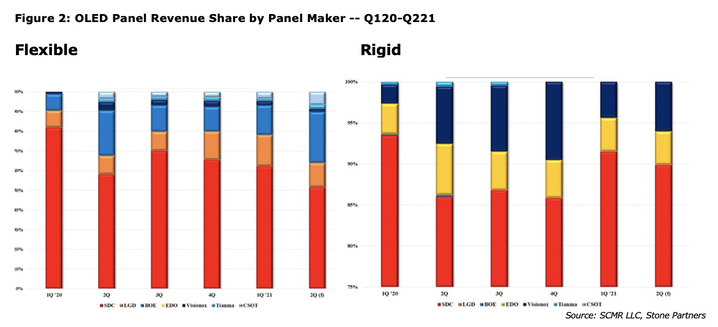

Samsung Display retained the largest share of OLED panel production although it has declined over the last five quarters dropping from 81.7% in Q120 to a forecasted 51.5% in Q221. Samsung and LG Display’s combined share of flexible OLED panel production declined from 90.3% in Q120 to (forecasted) 63.9% in Q221. Chinese flexible OLED panel producers rose from 9.7% in Q120 to 36.1% in Q221,

Neither LG Display nor BOE produces almost no rigid OLED panels, leaving the market almost exclusively to Samsung Display, EverDisplay and Tianma. Here again, Samsung Display’s share has declined from 93.5% in Q120 to 89.9% in Q221, a far smaller decline than seen in flexible displays. Combining flexible and rigid OLED production, Samsung Display’s dominance is even more obvious here, although its share dropped from 88.3% in Q120 to 71.1% in Q221.

Samsung Display retained the largest share of OLED panel production although it has declined over the last five quarters dropping from 81.7% in Q120 to a forecasted 51.5% in Q221. Samsung and LG Display’s combined share of flexible OLED panel production declined from 90.3% in Q120 to (forecasted) 63.9% in Q221. Chinese flexible OLED panel producers rose from 9.7% in Q120 to 36.1% in Q221,

Neither LG Display nor BOE produces almost no rigid OLED panels, leaving the market almost exclusively to Samsung Display, EverDisplay and Tianma. Here again, Samsung Display’s share has declined from 93.5% in Q120 to 89.9% in Q221, a far smaller decline than seen in flexible displays. Combining flexible and rigid OLED production, Samsung Display’s dominance is even more obvious here, although its share dropped from 88.3% in Q120 to 71.1% in Q221.

Although flexible OLEDs gather the most interest, the share in terms of sq. m of shipped displays between flexible and rigid has been evenly balanced and is likely to shift to rigid as OLEDs move to IT applications.