Vertical Divider

|

Samsung to Increase Use of LCDs for Low End Smartphones

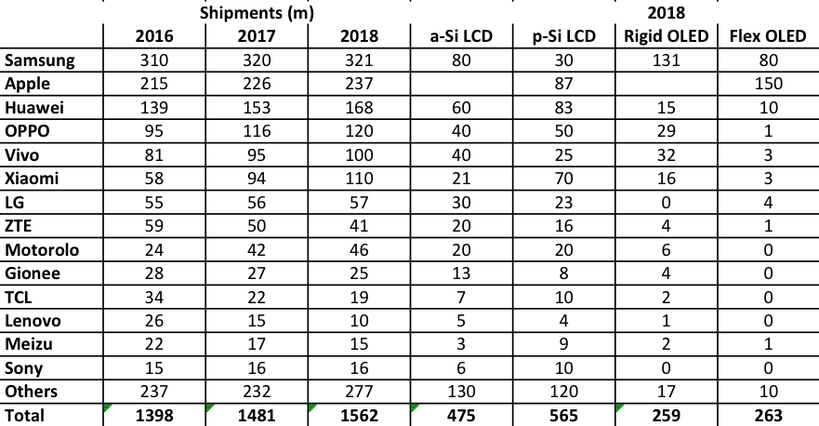

November 12, 2018 Samsung Mobile has been losing share to Chinese smartphone brands, who have been able to offer smartphones that are ‘almost’ as fully featured as Samsung’s, but sell for far less, resulting in a deterioration of Samsung’s share in China, while Xiaomi, Huawei, Vivo and OPPO share increased steadily. Samsung recently changed its stance on mid-range and low-end smartphones, and has begun to push new features and technology to the middle tier lines, rather than saving those improvements for new flagship Galaxy S series phones. In 2018, Samsung is expected to use OLEDs for 91% of its smartphones and LCDs for 9%. Samsung is expected to release an LCD based smartphone in its Galaxy A line, one that has been exclusively OLED based since the Galaxy A3, released in late 2015. The ‘A’ line of smartphones have ranged in price from ~$230 to ~$460, putting them squarely in the low to mid-range price category, and while every Galaxy A model will not use LCDs, there will likely be an allocation between LCD and OLED by region, with the LCD display models going to those regions where ASPs are lower, likely India and similar regional markets, while maintaining OLED displays in other markets. Cost is likely the greatest factor in Samsung’s decision, as on an absolute basis. However, using rigid OLED substrates, rather than the flexible substrates used in high-end devices, brings the cost of OLED displays to near parity with LCD, which would question the decision to use LCDs unless, of course, they were using a-Si and not p-Si. |

|

Table 1: Smartphone Shipments & Display Technology Breakdown

Source: IHS, OLED-A

At the same time, Huawei, Xiaomi, OPPO and Vivo are taking an opposite tack by increasing their use of OLEDs. Looking at 2018 for smartphones shipment reached 1.6b up 5% Y/Y and OLED panels were 33.4% of the total, split almost evenly between rigid and flexible.

The next set of table’s shows the display providers for the major Chinese smartphone OEMs, Huawei, Xiaomi, OPPO and Vivo for 2016-2018 and the split between a-Si LCDs, p-Si LCDs, OLEDs and Oxide LCDs. IN 2018, OPPO and Vivo used 32.8m and 31.0m OLED displays, respectively. These displays were primarily rigid. Huawei and Xiaomi use OLEDs in only 10.1m and 5.0m respectively. Tianma was the leading display supplier to Huawei and Xiaomi, while JDI was the #1 supplier for OPPO and JDI was #1 for Vivo. In both cases, Tianma was #2 or #3.

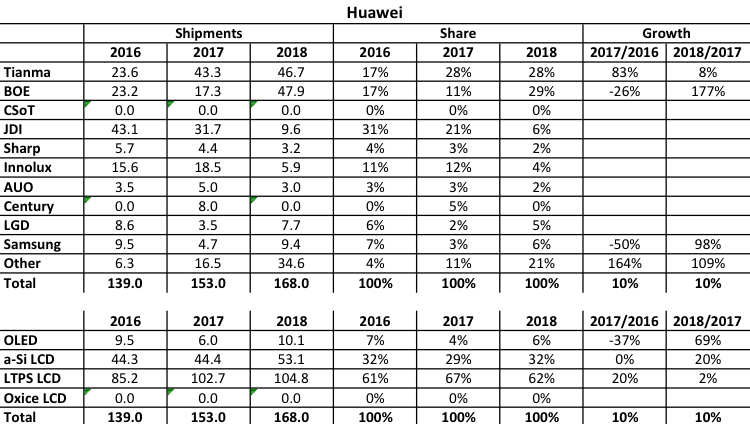

Table 2: Huawei Shipments, Share and Growth; Display Technology

The next set of table’s shows the display providers for the major Chinese smartphone OEMs, Huawei, Xiaomi, OPPO and Vivo for 2016-2018 and the split between a-Si LCDs, p-Si LCDs, OLEDs and Oxide LCDs. IN 2018, OPPO and Vivo used 32.8m and 31.0m OLED displays, respectively. These displays were primarily rigid. Huawei and Xiaomi use OLEDs in only 10.1m and 5.0m respectively. Tianma was the leading display supplier to Huawei and Xiaomi, while JDI was the #1 supplier for OPPO and JDI was #1 for Vivo. In both cases, Tianma was #2 or #3.

Table 2: Huawei Shipments, Share and Growth; Display Technology

Source: IHS, OLED-A

Table 3: Xiaomi Shipments, Share and Growth; Display Technology

Source: IHS, OLED-A

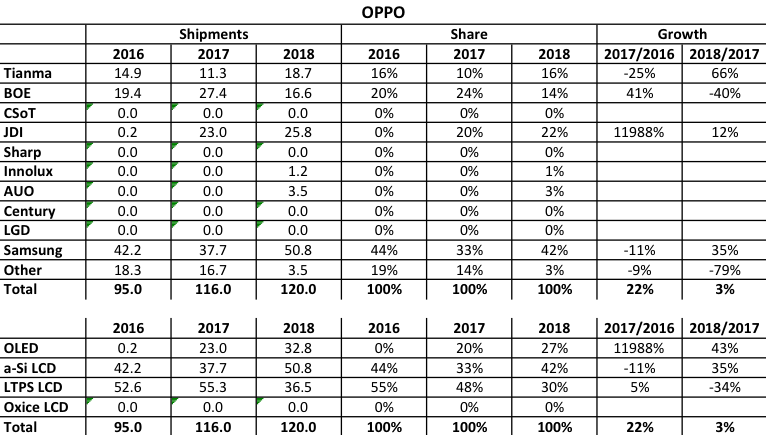

Table 4: OPPO Shipments, Share and Growth; Display Technology

Source: IHS, OLED-A

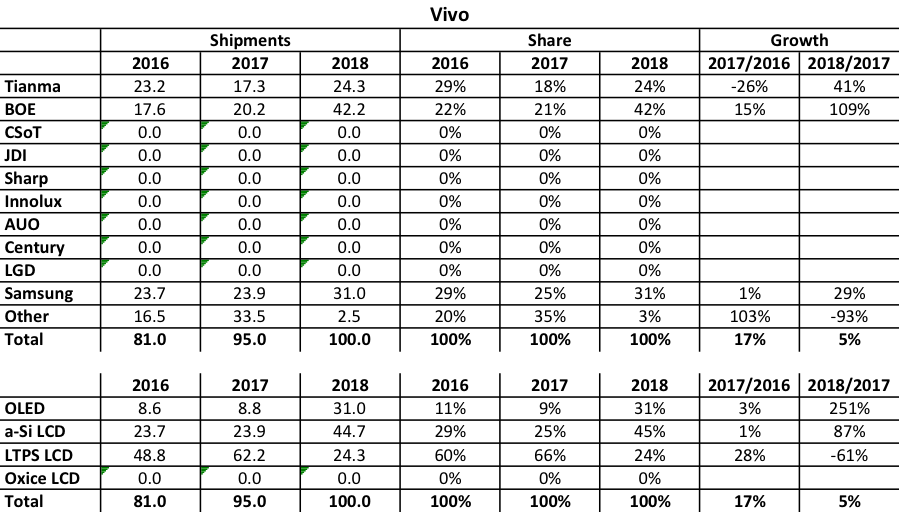

Table 5: Vivo Shipments, Share and Growth; Display Technology

Source: IHS, OLED-A