Vertical Divider

|

Special Musing Report

Samsung Formally Commits to QD/OLED Program of $11.0b October 11, 2019 In, 2013, Tim Cook speaking at a Goldman Sachs conference, said color saturation of OLED displays was “awful”. Four years later Apple introduced the first iPhone with an OLED display. Two of three new iPhones use OLEDs and it might have been 3 of 3, if not for a decision, possibly a result of the statement, to prop up a small Japanese LCD maker, JDI, with over $1b in prepayments. JDI’s recent confrontation with bankruptcy caused Apple to ignore the benefits of rigid low cost OLEDs and design LCDs into their low end phones; the only way to recover their investment. Soon, Kim, Hyun Suk, CEO of Samsung Electronics and Head, Visual Display Business will be put in a similar position. He has been highly critical OLED TVs in order to promote QLED TVs. Co-CEO Kim recently advocated to the Samsung Chairman to invest in Micro LED technology instead of OLEDs, but lost the argument. |

|

As expected, Samsung Display formally announced its QD/OLED investment of KRW 13.1t ($10.98b US) in fab construction and R&D through 2025. The announcement states that “Q1”, the company’s first production line of this type, is scheduled for 2021 and will be a Gen 8.5 fab with a phase 1 capacity of 30,000 sheets/month. Its current Gen 8.5 LCD production will be converted at the Asan, South Korea campus, and current LCD workers will be shifted to the new production facility, along with the hiring of an additional 81,000 workers over 5 years. Given that Samsung is closing all of their LCD lines, they will have plenty of employees to select from. SDC will also develop a supply chain specific that will include inkjet printing and material development along with a Display Research Center in conjunction with Korean Universities. The announcement did not mention, OLEDs, probably a concession to Samsung Visual, which still has to sell QLED (LCD) at least until 2021.

SDC’s L8-1 LCD line had a capacity of 120,000 sheets/month with room to spare. The converted line will have a capacity of 30,000 sheets/month initially, but could expand to 40,000 sheets/month. The line will use 2 Canon linear deposition tools at ~$300m-$400m each, as the IGZO backplane will be cut in two before the deposition process. SDC is evaluating Kateeva and SEMES tools in the pilot operation for ink-jet printing and organic encapsulation. The QD ink-jet printing costs will run between ~$500m and $600 (5 units) and another ~$300m to $400m for the encapsulation IJPs. SEMES is a $2b Samsung Electronics subsidiary (91.5% ownership) that specializes in Semiconductor and display equipment, particularly coater, etchers, and Ink-jet printers (display). Kateeva’s ink-jet printer is used for TFE by all the OLED fabs producing flexible displays, and has investments from Samsung, TCL, BOE, Veeco, Applied Materials and several VCs. The mass production decision would entail closing L8-2, currently a slightly larger Gen 8.5 LCD production line, which would then be converted into another QD/OLED line with at least another 30,000 sheet/month line with production probably starting in 2023.

SDC’s initial line should have a raw capacity of between 1.1m and 1.3m large area panels/year, but actual output will depend on the yield and utilization. SDC will likely produce a small number of panels on the pilot line for CES 2020, but will begin full production on the Q1 line in early 2021, and if the decision is made to build out the Q2 line in 2Q 2020, SDC could have the 2nd line in mass production by late 2022. Production will focus on 65” panels (3 -up) and migrating to 77” (2-up), and the line will employ MMG (Multi-mode glass), to increase the efficiency of substrate use.

Why is Samsung spending almost $11b to produce a new TV technology in a market that is already over-saturated?

In 2013, Samsung chose not to pursue the development of large OLED panels, due in large part to the failure of their chosen approach, LTPS backplanes and FMM mask deposition tools, to meet the cost expectations. The FMM mask deposition tool was only able to handle 1/6thof a Gen 8.5 substrate and was a key cost inflator. By comparison, LG Display successfully used a ½ Gen 8.5 linear deposition tool with open masks for RGBW and lower cost IGZO backplanes, to produce white light with a CFOA.

Samsung’s response to the setback was to replace yellow phosphor with quantum dot films on the LED backlight to enhance the color purity of their LCD TVs, but while they were able to achieve better color than LED/phosphor backlights and marginally improved CR, the “QLED” TVs were inferior to OLEDs in contrast ratio, viewing angle readability, form factor, (thinness), response time and power consumption. Samsung tried to overcome some of these limitation by adding compensation films for wider viewing angles and faster LCs. But each change was a tradeoff in performance. Even the expected advantage of higher luminance has proven to be a myth in viewing real world videos, where measurements show the resulting luminance of OLEDs and QD LCDs with 70% higher spec’d luminance to be the same. Samsung convinced many consumers to buy QLED TVs, but they did not impact LGE and the other 16 TV brands from selling all the OLED panels that LGD could produce, even though OLEDs led to higher price points for the OLED TVs.

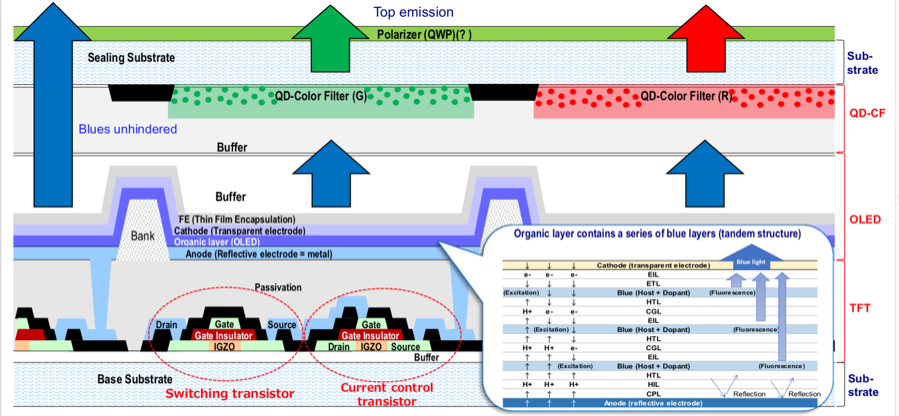

SDC’s QD/OLED panels will use 3 blue OLED emitter layers, which are deposited using an open-mask, eliminating the need for fine metal masks as shown below. The TFT circuitry that drives the OLED material is produced using IGZO, which is an upgrade to the a-Si line used for LCDs. The blue photons created by the OLEDs will be converted to red and green by the printed QDs with the blue light passing thru a transparent layer. This approach is different from the QD films used in LCDs, where the blue light from the LEDs passes thru a combined film of red and green QDs. The QD density in the film is engineered to allow approximately ~33% of the photons to pass thru the film without hitting a QD and therefore maintain the blue color. In the QD/OLED design, the separate red and green QDs are designed with a density that cause most of the photons to hit a QD to achieve the desired efficacy. However, the efficacy will still be impacted by ~90% absorption, which means that ~10% of the photons hitting a QD are converted to heat instead of light.

Figure 1. Samsung’s QD/OLED Architecture

SDC’s L8-1 LCD line had a capacity of 120,000 sheets/month with room to spare. The converted line will have a capacity of 30,000 sheets/month initially, but could expand to 40,000 sheets/month. The line will use 2 Canon linear deposition tools at ~$300m-$400m each, as the IGZO backplane will be cut in two before the deposition process. SDC is evaluating Kateeva and SEMES tools in the pilot operation for ink-jet printing and organic encapsulation. The QD ink-jet printing costs will run between ~$500m and $600 (5 units) and another ~$300m to $400m for the encapsulation IJPs. SEMES is a $2b Samsung Electronics subsidiary (91.5% ownership) that specializes in Semiconductor and display equipment, particularly coater, etchers, and Ink-jet printers (display). Kateeva’s ink-jet printer is used for TFE by all the OLED fabs producing flexible displays, and has investments from Samsung, TCL, BOE, Veeco, Applied Materials and several VCs. The mass production decision would entail closing L8-2, currently a slightly larger Gen 8.5 LCD production line, which would then be converted into another QD/OLED line with at least another 30,000 sheet/month line with production probably starting in 2023.

SDC’s initial line should have a raw capacity of between 1.1m and 1.3m large area panels/year, but actual output will depend on the yield and utilization. SDC will likely produce a small number of panels on the pilot line for CES 2020, but will begin full production on the Q1 line in early 2021, and if the decision is made to build out the Q2 line in 2Q 2020, SDC could have the 2nd line in mass production by late 2022. Production will focus on 65” panels (3 -up) and migrating to 77” (2-up), and the line will employ MMG (Multi-mode glass), to increase the efficiency of substrate use.

Why is Samsung spending almost $11b to produce a new TV technology in a market that is already over-saturated?

In 2013, Samsung chose not to pursue the development of large OLED panels, due in large part to the failure of their chosen approach, LTPS backplanes and FMM mask deposition tools, to meet the cost expectations. The FMM mask deposition tool was only able to handle 1/6thof a Gen 8.5 substrate and was a key cost inflator. By comparison, LG Display successfully used a ½ Gen 8.5 linear deposition tool with open masks for RGBW and lower cost IGZO backplanes, to produce white light with a CFOA.

Samsung’s response to the setback was to replace yellow phosphor with quantum dot films on the LED backlight to enhance the color purity of their LCD TVs, but while they were able to achieve better color than LED/phosphor backlights and marginally improved CR, the “QLED” TVs were inferior to OLEDs in contrast ratio, viewing angle readability, form factor, (thinness), response time and power consumption. Samsung tried to overcome some of these limitation by adding compensation films for wider viewing angles and faster LCs. But each change was a tradeoff in performance. Even the expected advantage of higher luminance has proven to be a myth in viewing real world videos, where measurements show the resulting luminance of OLEDs and QD LCDs with 70% higher spec’d luminance to be the same. Samsung convinced many consumers to buy QLED TVs, but they did not impact LGE and the other 16 TV brands from selling all the OLED panels that LGD could produce, even though OLEDs led to higher price points for the OLED TVs.

SDC’s QD/OLED panels will use 3 blue OLED emitter layers, which are deposited using an open-mask, eliminating the need for fine metal masks as shown below. The TFT circuitry that drives the OLED material is produced using IGZO, which is an upgrade to the a-Si line used for LCDs. The blue photons created by the OLEDs will be converted to red and green by the printed QDs with the blue light passing thru a transparent layer. This approach is different from the QD films used in LCDs, where the blue light from the LEDs passes thru a combined film of red and green QDs. The QD density in the film is engineered to allow approximately ~33% of the photons to pass thru the film without hitting a QD and therefore maintain the blue color. In the QD/OLED design, the separate red and green QDs are designed with a density that cause most of the photons to hit a QD to achieve the desired efficacy. However, the efficacy will still be impacted by ~90% absorption, which means that ~10% of the photons hitting a QD are converted to heat instead of light.

Figure 1. Samsung’s QD/OLED Architecture

Source: Mizuho Securities Equity Research

Samsung must also decide whether to use a color filter or a polarizer to inhibit the ambient light from hitting the QDs and to improve the contrast ratio, according to Nanosys. Given this configuration and the current use of 12-15 masks for the IGZO process and the need to lay down 3 full organic layers plus the use of 5 IJPs, the anticipated cost advantage over the LG Display approach is probably non-existent. Also, if a color filter or polarizer is needed the luminance advantage would be lost. Samsung’s image sticking campaign against OLED TVs could also come back to haunt the company. Image sticking is caused by the high use and therefore the aging of specific sub-pixels. Since, Samsung uses blue OLED material, which has by orders of magnitude the shortest lifetime of OLED emitters (LG uses blue, red and yellow-green), the QD/OLED design is susceptible to faster aging than the LG design. Samsung is apparently using an aging compensation technique similar to what Canadian-based IGNIS innovation developed to offset the aging process.

Finally, LG Display’s next OLED fab will be a Gen 10.5 and that will put more pressure on Samsung, since a Gen 10.5 substrate produces 8 65” panels with 94% glass usage efficiency, while a Gen 8.5 produces 3 65” panels at 64% glass efficiency. MMG helps to offset the difference but the smaller panels don’t generate the price/area of the 65” displays.

Finally, LG Display’s next OLED fab will be a Gen 10.5 and that will put more pressure on Samsung, since a Gen 10.5 substrate produces 8 65” panels with 94% glass usage efficiency, while a Gen 8.5 produces 3 65” panels at 64% glass efficiency. MMG helps to offset the difference but the smaller panels don’t generate the price/area of the 65” displays.