Vertical Divider

|

Samsung Electronics Q317 Revenue up 30% and Operating Profits up 179% Y/Y

November 06, 2017 Samsung Electronics sales were pretty good, driven by their chip business and got a little boost from OLEDs, as previously announced. Profitability across segments other than memory and OLEDs were not as good.

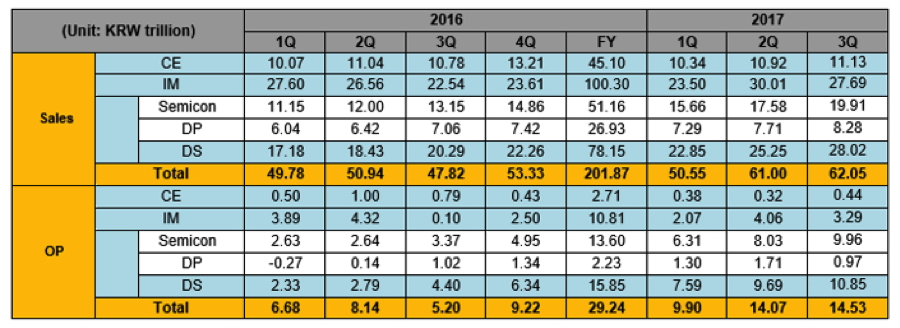

Table 1: Samsung Revenue & Operating Market by Business Unit

Source: Company Data

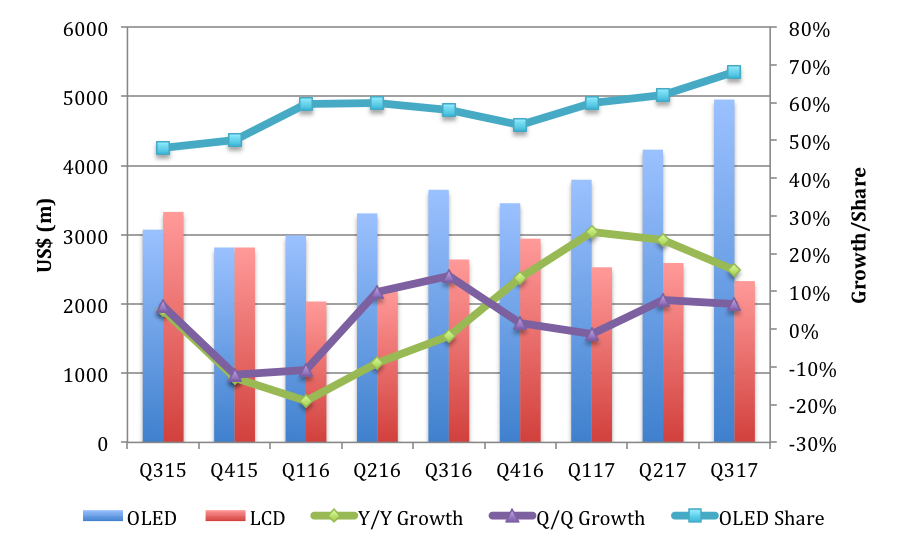

Samsung Display posted KRW 8.28 trillion in consolidated revenue and KRW 0.97 in profits up 7% Q/Q and 16% Y/Y. OLEDs grew to 67% of total display revenues. Once again, OLEDs drove the quarter with OLED up 15% Q/Q and 37% Y/Y on strong demand from the Galaxy S8 and Note 8 OLED displays. Figure 1: Samsung’s OLED and LCD Revenue and Growth

Source: DSCC, OLED-A

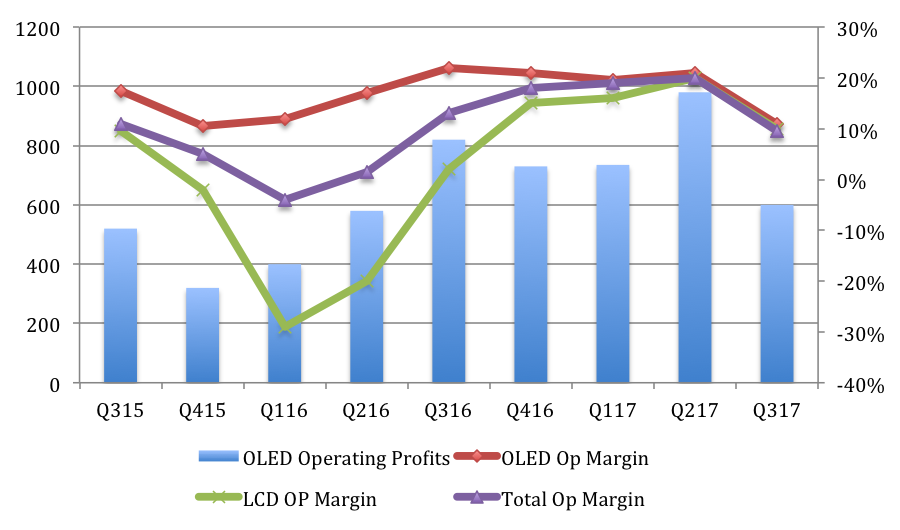

The bad news was that Samsung’s OLED fab utilization apparently fell from the mid-80% range in Q2 to the mid-70% range even as OLED display demand increased in China. Reportedly, there were some yield issues from new cover glass OCA lamination material that are now solved, but caused a reduction in supply. Other reports indicated that only 20m iPhone X will ship in 2017 down from an expected 50m. As a result, OLED operating income fell 37% Q/Q and 27% Y/Y to $609M. It was their first Y/Y decline in OLED operating income that we are aware of. In addition to the reduced utilization and yield issues, increased price competition for rigid OLEDs vs. LTPS LCDs also contributed to the shortfall as did some Chinese brands adjustments in order timing. As a result, OLED operating margins fell from 22.5% in Q2’17 to 12.4% in Q3’17 as shown in Figure 5. However, OLEDs still contributed the dominant share of their operating profits at 71%. LCD revenues were down 6% Q/Q and 12% Y/Y as demand stalled for TV panels from elevated panel and street prices forcing TV panel prices down significantly. LCD operating income was down 55% Q/Q to $247M, the lowest since Q3'16. LCDs contributed to just 29% of display operating income and LCD operating margins fell from 21.7% to 10.4%. Figure 2: Samsung’s OLED and LCD Operating Margins

Source: DSCC, OLED-A

In the case of OLEDs, profitability will likely rebound quickly as the iPhone X’s constraints are overcome and utilization and yield improve. Flexible OLEDs with their higher ASPs and margins should gains share and its OLED operating margins will likely return to over 20%. In terms of Capex, Samsung reduced their display capex by 40% Q/Q to US$2.3b down from US$4.0b in in Q2’17. The company also guided to $12.3B for the year, which implies another decline of 4% to $2.3B in Q4’17. Samsung may have pushed some spending out by a couple of months due to the lower than expected utilization in Q3’17 and Apple’s slower than expected ramp. In summary: Display OLEDs

Mobile

TV

4Q

2018

Samsung Electronics is facing the same issues that most other CE brands are facing, and while they have the small panel OLED business to keep things moving, that business, or at least a segment of that business (rigid small panel OLED) is facing enough competition from traditional small panel LCD that it is affecting overall OLED profitability. This competition is expected, given the enormous infrastructure investments that have been made in LCD over the years, and investors who expect the LCD display segment to shut down because Samsung Display has closed a few old lines, are mistaken. Samsung isn’t expecting OLED significant OLED competition until 2019 at the earliest. (This article is based on reports from both DSCC and SCMR) |

|