Vertical Divider

Q121 Advanced TV Shipments up 70% Y/Y to 3.8m

The term Advanced TV (ATV) shipments was created by DSCC and has now been widely adopted by market research firms including Omdia. DSCC defines the term, essentially as any TV that uses QD enhanced backlights or OLED technology. As a result, the definition includes TVs that offer little in the way pf advanced features as long as they have a QD based backlight.

DSCC reports Q1 2021 ATVs jumped by 70% Y/Y to 3.8M units. Advanced LCD TVs of 75” increased 158% Y/Y to 336K, and Advanced LCD TVs larger than 75” increased 103% to 123K, while OLED TVs 77” and larger increased by 430% to 85K, more than the total cumulative volume of this category for all years up to the end of 2019. OLED TVs share of all Advanced TV declined during 2018-2020 as the category had a very liberal definition, LG Display’s Guangzhou fab, which opened in Q420 and doubled the monthly OLED TV shipment capacity increased by 97% Y/Y in Q1 2021, while Advanced LCD TV shipments increased by 61% Y/Y. The OLED TV share increased from 26% in Q1 2020 to 30% in Q1 2021.

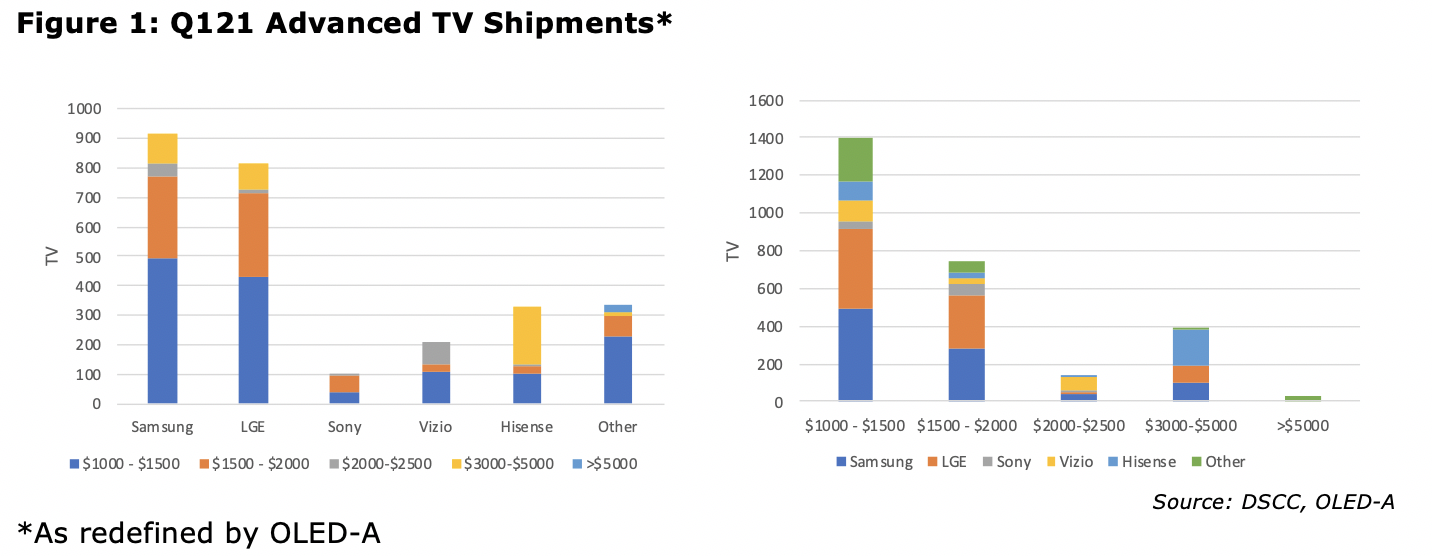

Taking a more conservative view of the definition of Advanced TV by eliminating the <$1,000 category, LGE and Samsung were close in shipment volume in Q121 with 34% and 30% shares respectively and the leading shipment volume by way of price was $1000 to $1500 with a 52% share.

The term Advanced TV (ATV) shipments was created by DSCC and has now been widely adopted by market research firms including Omdia. DSCC defines the term, essentially as any TV that uses QD enhanced backlights or OLED technology. As a result, the definition includes TVs that offer little in the way pf advanced features as long as they have a QD based backlight.

DSCC reports Q1 2021 ATVs jumped by 70% Y/Y to 3.8M units. Advanced LCD TVs of 75” increased 158% Y/Y to 336K, and Advanced LCD TVs larger than 75” increased 103% to 123K, while OLED TVs 77” and larger increased by 430% to 85K, more than the total cumulative volume of this category for all years up to the end of 2019. OLED TVs share of all Advanced TV declined during 2018-2020 as the category had a very liberal definition, LG Display’s Guangzhou fab, which opened in Q420 and doubled the monthly OLED TV shipment capacity increased by 97% Y/Y in Q1 2021, while Advanced LCD TV shipments increased by 61% Y/Y. The OLED TV share increased from 26% in Q1 2020 to 30% in Q1 2021.

Taking a more conservative view of the definition of Advanced TV by eliminating the <$1,000 category, LGE and Samsung were close in shipment volume in Q121 with 34% and 30% shares respectively and the leading shipment volume by way of price was $1000 to $1500 with a 52% share.