Vertical Divider

|

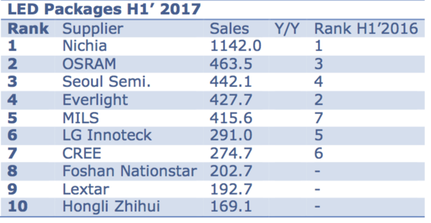

Nichia Continues to Lead in LED Package Revenues

October 23, 2017 Japan-based Nichia recorded the highest revenues among all main LED packaging service providers worldwide in first-half 2017, with sales reaching JPY132.79 billion (US$1.142 billion), up 4.9% on year, according to Digitimes Research. Germany-based Osram Opto Semiconductors ranked second with US$463.5 million, up 11.1% on year. Third-place Korea-based Seoul Semiconductor had US$442.1 million, up 12.1%, followed by Taiwan's Everlight Electronics with US$427.7 million, down 2.8%. The other major players' revenues for the period were: China-based MLS, US$415.6 million, up 66.3%; Korea-based LG Innotek, US$291.0 million, down 4.1%; US-based Cree, 274.7 million, down 11.2%; China-based Foshan Nationstar Optoelectronics, US$202.7 million, up 50.0%; Taiwan's Lextar Electronics, US$192.7 million, down 11.7%; and China's Hongli Zhihui, US$169.1 million, up 65.4%. The China-based makers' significant revenue growths were driven by major production capacity expansions. After rampant government sponsored expansion in 2011/2012 and an oversupply crash that closed a significant number of Chinese LED producers and packagers, the ‘2nd wave’ of expansion seems to have taken hold as indicated by the table below. Digitimes has ranked the top LED packagers for 1H 2017, and while Japan based Nichia retained the top position with a 4.9% revenue gain, the biggest gainers were the three Chinese packagers who all saw revenue gains at 50% or above. This was driven by capacity expansion, which in this cycle (thus far) has done much less pricing damage. That said, LED bulb pricing is still on the decline as seen by the charts below, despite higher LED lighting penetration rates, but TV backlight demand from the display space, and automotive demand have helped to slow declines to more manageable levels and both LED and bulb pricing has been showing far more stability than in previous build cycles. While it is difficult to determine whether the industry has matured enough not to expand at a rate far in excess of industry growth, or whether a more reasonable financial incentive policy in China has taken hold, it’s a good thing, but with Chinese growth rates so much higher than other regions, it will be difficult for others to follow the share based approach of Chinese packagers. Focusing on profitability will likely be far more important to non-Chinese packagers over the mid-term, and would be the only way they would be able to maintain themselves should we see a cyclical downturn in demand over the next few years. Table 1 - LED Packagers 1H 2017

Source: Digitimes Research and OLED-A

|

|