Vertical Divider

LCD Large Panel Revenue Up 65.6% Y/Y

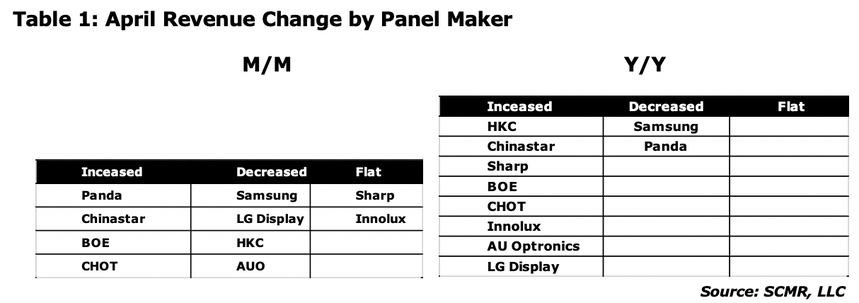

Large panel LCD revenue saw a sequential decline of 2.1% in April after a large increase in March. Large panel shipments declined 6.6% sequentially but large panel ASP increased by 4.8% offsetting much of the unit volume decline. Y/Y the large panel segment was up 65.6%. On a regional basis the industry saw growth in large panel sales in only one region, China, where sales were up 4.0% sequentially and up 82.1% Y/Y. On a weighted average basis, the industry declined 1.5% in revenue in April, but was up 50.6% Y/Y.

Panel producers remain in an advantageous position, with demand outstripping supply, but the ASP increases seen each month must be maintained going forward as shipments decline, a result of component shortages, with mix shift limited by those same shortages. Large panel sales have declined each month this year other than March, which saw a large (13.4%) increase as the New Year holiday in China ended and inventory needed to be replenished. Large panel demand has remained strong enough to offset component shortage based delivery push-outs, but at the first sign of weaker demand, panel producers will begin to see their absolute control over panel pricing erode. Even with relatively flat unit volumes, panel producers have been able to show very strong Y/Y results but will see those comparisons getting more difficult for the remainder of the year.

Large panel LCD revenue saw a sequential decline of 2.1% in April after a large increase in March. Large panel shipments declined 6.6% sequentially but large panel ASP increased by 4.8% offsetting much of the unit volume decline. Y/Y the large panel segment was up 65.6%. On a regional basis the industry saw growth in large panel sales in only one region, China, where sales were up 4.0% sequentially and up 82.1% Y/Y. On a weighted average basis, the industry declined 1.5% in revenue in April, but was up 50.6% Y/Y.

Panel producers remain in an advantageous position, with demand outstripping supply, but the ASP increases seen each month must be maintained going forward as shipments decline, a result of component shortages, with mix shift limited by those same shortages. Large panel sales have declined each month this year other than March, which saw a large (13.4%) increase as the New Year holiday in China ended and inventory needed to be replenished. Large panel demand has remained strong enough to offset component shortage based delivery push-outs, but at the first sign of weaker demand, panel producers will begin to see their absolute control over panel pricing erode. Even with relatively flat unit volumes, panel producers have been able to show very strong Y/Y results but will see those comparisons getting more difficult for the remainder of the year.

2/3rds of the Way through the 2nd quarter panel prices continue their rapid increases with only a few exceptions.

North America has been the growth leader in the TV market, with stimulus checks and continued stay-at-home attitudes keeping demand high, especially relative to China and Europe, where demand is weaker, but as COVID-19 restrictions are lifted, and TV set prices continue to rise, demand will slow, which it did in April. There are still TV stock outs at TV retailers in the US, as panel supply is constrained by component shortages, but continued upward pressure on set prices as a potential factor could change the positive outlook that set makes still seem to have.

2/3rds of the Way through the 2nd quarter panel prices continue their rapid increases with only a few exceptions. Monitor panel prices increased by 5.8%, almost identical to the previous month and the average monthly increase (5.7%) seen so far this year. Monitor demand continues to be strong enough to support price increases on a general basis, but shortages of a number of components, particularly controllers, allow panel producers to remain in a favorable bargaining position which has allowed them to offset lower unit volume with higher prices. The aggregated current price for monitors is currently 24.4% above the high point last year and 51.5% above the low (see Fig. 5 for earlier years).

Notebook panel prices increased by 3.9% in May, a bit below the previous month’s gain, but again, almost on the average gain for this year of 3.7%. Demand also continues to be strong, led by a number of global educational purchase programs that have continued this year, and the same component issues as mentioned above. While we expect some of those high volume purchase programs to end by the end of 2Q, the component shortages have pushed out delivery for panels and extended lead times for notebook delivery, which could extend demand strength into the summer a bit.

Aggregate TV panel pricing was up 3.7% in May, showing a much lower increase than last month (7.3%) and lower than the average increase so far this year (5.6%). While calling a 3.7% monthly increase might be overstating the facts, given the last 12 months, especially the last 6 or 7 months, the increase was unusually low, and while TVs face the same or greater semiconductor related shortages as other panels, the aggregate price of TV panels is now up 28.7% from last year’s highest point and up 107.3% above last year’s low. TV set producers have increased set prices at least once this year, with some twice, and are worried that another price increase, which seems inevitable will begin to have a more significant impact on demand.

North America has been the growth leader in the TV market, with stimulus checks and continued stay-at-home attitudes keeping demand high, especially relative to China and Europe, where demand is weaker, but as COVID-19 restrictions are lifted, and TV set prices continue to rise, we expect demand to slow, which it did in April. There are still TV stock outs at TV retailers in the US, as panel supply is constrained by component shortages, but we see the continued upward pressure on set prices as a potential factor that could change the positive outlook that set makes still seem to have.

While we have not seen any major changes to TV set yearly targets, the somewhat bleak outlook for any significant change in semiconductor supply leads us to expect that component shortages will continue into 3Q, which will limit panel volume and keep upward pressure on TV panel prices, which will have an increasing effect on demand. Whether May’s ‘weaker’ panel price increase reflects a shift in TV set demand is moot as one month certainly does not make a trend, but should we see a lower rate of change continue, it could signal a change in demand over the next few months. A bit too early to tell, but certainly a possibility.

Mobile phone panel prices did not change in May, and while that would be below this year’s average increase of 1.2%, mobile phone panel prices have been much more stable than other categories. While demand spikes do occur when new release inventory building arises, smartphone demand has not seen the increases that other CE product categories have this year, and Chinese demand is beginning to look like it is resuming its more typical weaker trend, with April seeing negative y/y growth after positive y/y growth in the 1stquarter. The COVID-19 issues in India are also a drag on smartphone demand, all of which give us the view that mobile panel prices will see relatively mild increases in 2Q overall and potentially for the remainder of the year, other than the typical seasonal spike in September.

- Monitor panel prices increased by 5.8%, almost identical to the previous month and the average monthly increase (5.7%) seen so far this year. Monitor demand continues to be strong enough to support price increases on a general basis, but shortages of a number of components, particularly controllers, allow panel producers to remain in a favorable bargaining position which has allowed them to offset lower unit volume with higher prices. The aggregated current price for monitors is currently 24.4% above the high point last year and 51.5% above the low.

- Notebook panel prices increased by 3.9% in May, a bit below the previous month’s gain, but again, almost on the average gain for this year of 3.7%. Demand also continues to be strong, led by a number of global educational purchase programs that have continued this year, and the same component issues as mentioned above. While we expect some of those high volume purchase programs to end by the end of 2Q, the component shortages have pushed out delivery for panels and extended lead times for notebook delivery, which could extend demand strength into the summer a bit.

- Aggregate TV panel pricing was up 3.7% in May, showing a much lower increase than last month (7.3%) and lower than the average increase so far this year (5.6%). While TV products have the same or greater semiconductor related shortages as other panels, the aggregate price of TV panels is now up 28.7% from last year’s highest point and up 107.3% above last year’s low. TV set producers have increased set prices at least once this year, with some twice, and are concerned that another price increase will slow demand

- Mobile phone panel prices were flat in May, and while that would be below this year’s average increase of 1.2%, mobile phone panel prices have been much more stable than other categories. The COVID-19 issues in India are also a drag on low end smartphone demand but are insufficient to change the price dynamics for OLEDs.

North America has been the growth leader in the TV market, with stimulus checks and continued stay-at-home attitudes keeping demand high, especially relative to China and Europe, where demand is weaker, but as COVID-19 restrictions are lifted, and TV set prices continue to rise, demand will slow, which it did in April. There are still TV stock outs at TV retailers in the US, as panel supply is constrained by component shortages, but continued upward pressure on set prices as a potential factor could change the positive outlook that set makes still seem to have.

2/3rds of the Way through the 2nd quarter panel prices continue their rapid increases with only a few exceptions. Monitor panel prices increased by 5.8%, almost identical to the previous month and the average monthly increase (5.7%) seen so far this year. Monitor demand continues to be strong enough to support price increases on a general basis, but shortages of a number of components, particularly controllers, allow panel producers to remain in a favorable bargaining position which has allowed them to offset lower unit volume with higher prices. The aggregated current price for monitors is currently 24.4% above the high point last year and 51.5% above the low (see Fig. 5 for earlier years).

Notebook panel prices increased by 3.9% in May, a bit below the previous month’s gain, but again, almost on the average gain for this year of 3.7%. Demand also continues to be strong, led by a number of global educational purchase programs that have continued this year, and the same component issues as mentioned above. While we expect some of those high volume purchase programs to end by the end of 2Q, the component shortages have pushed out delivery for panels and extended lead times for notebook delivery, which could extend demand strength into the summer a bit.

Aggregate TV panel pricing was up 3.7% in May, showing a much lower increase than last month (7.3%) and lower than the average increase so far this year (5.6%). While calling a 3.7% monthly increase might be overstating the facts, given the last 12 months, especially the last 6 or 7 months, the increase was unusually low, and while TVs face the same or greater semiconductor related shortages as other panels, the aggregate price of TV panels is now up 28.7% from last year’s highest point and up 107.3% above last year’s low. TV set producers have increased set prices at least once this year, with some twice, and are worried that another price increase, which seems inevitable will begin to have a more significant impact on demand.

North America has been the growth leader in the TV market, with stimulus checks and continued stay-at-home attitudes keeping demand high, especially relative to China and Europe, where demand is weaker, but as COVID-19 restrictions are lifted, and TV set prices continue to rise, we expect demand to slow, which it did in April. There are still TV stock outs at TV retailers in the US, as panel supply is constrained by component shortages, but we see the continued upward pressure on set prices as a potential factor that could change the positive outlook that set makes still seem to have.

While we have not seen any major changes to TV set yearly targets, the somewhat bleak outlook for any significant change in semiconductor supply leads us to expect that component shortages will continue into 3Q, which will limit panel volume and keep upward pressure on TV panel prices, which will have an increasing effect on demand. Whether May’s ‘weaker’ panel price increase reflects a shift in TV set demand is moot as one month certainly does not make a trend, but should we see a lower rate of change continue, it could signal a change in demand over the next few months. A bit too early to tell, but certainly a possibility.

Mobile phone panel prices did not change in May, and while that would be below this year’s average increase of 1.2%, mobile phone panel prices have been much more stable than other categories. While demand spikes do occur when new release inventory building arises, smartphone demand has not seen the increases that other CE product categories have this year, and Chinese demand is beginning to look like it is resuming its more typical weaker trend, with April seeing negative y/y growth after positive y/y growth in the 1stquarter. The COVID-19 issues in India are also a drag on smartphone demand, all of which give us the view that mobile panel prices will see relatively mild increases in 2Q overall and potentially for the remainder of the year, other than the typical seasonal spike in September.