Vertical Divider

|

KLA-Tencor Buys Orbotech

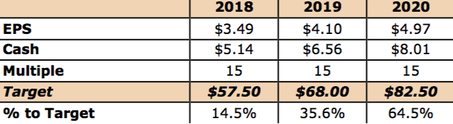

March 26, 2018 The managements of KLA-Tencor and Orbotech have agreed to a merger that values Orbotech at $3.4b through a combination of cash and KLA-Tencor stock ($38.86 and .25 shares of KLAC) which closed at $115.98, for a value of $67.86, a 13.3% premium to Orbotech’s closing price on the day before the deal was announced, and a 16.7% premium to Orbotech’s 10 day closing average. The deal includes a termination fee of $125m and does not allow for Orbotech to solicit a higher proposal although KLA-Tencor has the right to make another offer if Orbotech were to receive a legitimate unsolicited offer. The deal can be terminated by mutual agreement, if shareholder approval is not granted, or if government approval is not granted, and while no specific date has been set for the shareholder vote or closing, Orbotech management expects the deal to be closed before the end of this year. The deal has an ‘outstanding litigation limit’ of $25m and requires all accruals to be on the balance sheet. In May 2017 Orbotech received a ‘best judgment tax assessment’ from the Israeli Tax Authority with respect to an audit of the company for the fiscal years 2012 – 2014 in the amount of NIS $207m ($59.48m US currently). On 12/20/2017 the company issued a statement concerning the judgment and stated that the company had not taken any reserves or provisions against the levy. We would assume that the matter has been settled or reserves have been taken that will show in the 1Q 2018 balance sheet. On March 9, an Israeli paper had indicated that shareholders in Orbotech were in the US to discuss the sale of a controlling interest in the company, and that the company would be attractive to a tool vendor that would want to expand their share, especially given that Orbotech is the share leader in many of the markets it serves. KLA-Tencor has a broad product line of tools oriented toward semiconductor manufacturing that fit well with Orbotech’s yield management tools and semiconductor advanced packaging focus. Orbotech’s display segment will open a new market for KLAC, the company’s semiconductor processing tools are complementary to KLAC’s, and on a broad basis, the idea of automated inspection is common to both companies, but Orbotech’s repair (additive) technology would be new to KLAC’s tool portfolio. The companies expect $50m in synergies, which strikes us as a bit high as Orbotech is expected to remain a standalone company in Israel. Table 1: Orbotech Long-Term Price Targets

Source: SCMR LLC

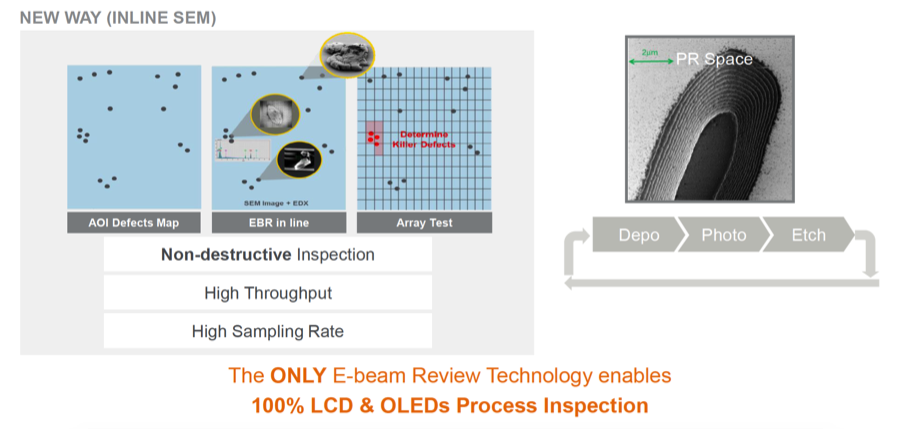

The merger adds to KLAC’s competitiveness with Applied Materials just as Applied expects to enter the Inspection and Repair Tool market. Figure 1: Applied's Inspection Method for Display

Source: Company

|

|