|

Flexible OLED Capacity Reduced by 12%, 30% and 22% in 2018-2020

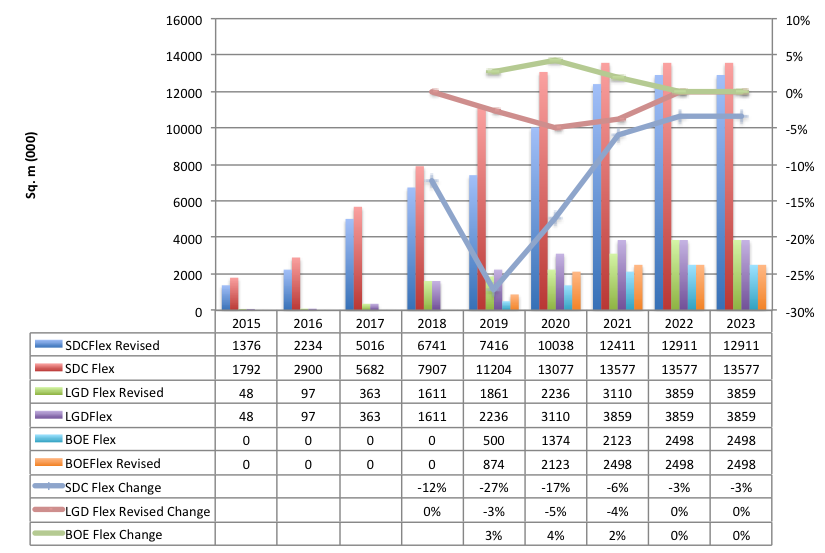

March 19, 2018 Last week, we discussed in depth the impact of Apple’s lower than expected sales of the iPhone X, which resulted in a deferment of OLED equipment purchases by LG and Samsung. Among the contenders for Apple’s business, is BOE (200725.CH), China’s largest panel producer and among the most aggressive toward OLED capacity expansion. The Chinese press reported that BOE, CSOT, Tianma, Everdisplay were filling the slowdown in Korean OLED capacity growth and other Chines panel makers. We reported that BOE signed a contract with SFA Engineering with a value of $143.6m, indicating a substantial number of tools. The contract will provide equipment for BOE’s B11 fab in Mianyang, China. This fab, which will have a raw capacity of 45,000 sheets when fully built out, and is expected to begin production in 3Q 2019 (phase 1), and would be BOE’s 2ndflexible OLED fab after the opening of their B7 flexible OLED fab in Chengdu last year, and relatively small rigid OLED production at their fab in Ordos. BOE also committed to building a flexible 6th Gen OLED fab in Chongqing. Taking a look at the changes, we compares the raw flexible capacity for LG and Samsung before the equipment ordering delays with BOE’s raw flexible capacity in the next figure. Samsung’s changes are the most significant, reducing total flexible capacity by 12%, 27% and 17% in 2018-2020. LG’s reductions are 3%, 5% and 4% between 2019 and 2021 and BOE is up 3%, 4% and 2% between 2019 and 2021 with the addition of the Chongqing fab. Even with the changes, Samsung’s capacity for flexible displays should never drop below 50%. Figure 1: OLED Raw Capacity Before and After Equipment Push-Outs

|

Vertical Divider

|

Source: OLED-A