Vertical Divider

Display Equipment Suppliers Produce Low Revenue with Y/Y Growth

The display equipment market for Korean companies has been a hit or miss proposition recently, with those supplying equipment to Chinese panel producers seeing delays, while those producing tools for advanced products seeing strong sales. Recently listed Shindo ENG seeing a sales drop of 58% Y/Y, a result of COVID-19 delays at new OLED projects in China, while K-Mac, a producer of display inspection systems saw a slight decrease in sales but a 78% increase in backlog in 1H20, as it is the main supplier of tools that measure the thickness of deposited films, such as those used in OLED displays.

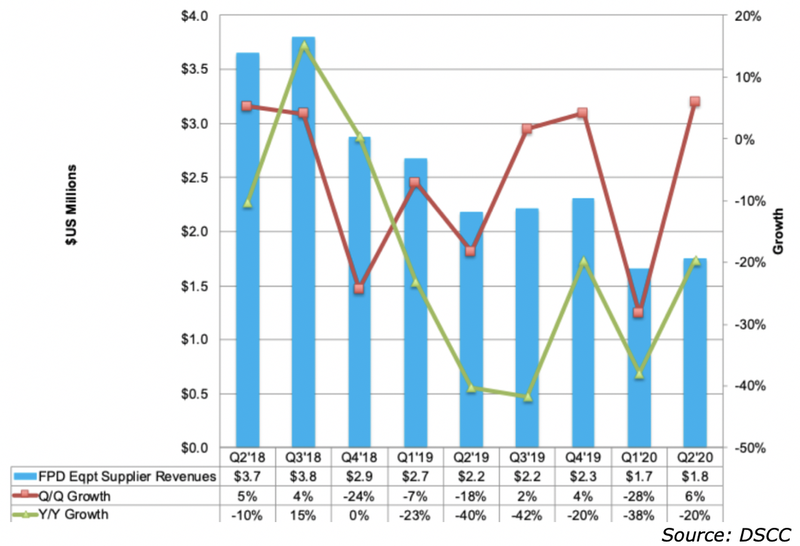

DSCC surveyed 35 display equipment companies including Applied Materials, AP Systems, Avaco, Canon (Tokki), Charm, Coherent, Contrel, Device ENG, DMS, EO Technics, Han's Laser, HB Technology, ICD, Invenia, Jusung, KC Tech, KMAC, LIS, Nikon, Nissin Electric, Philoptics, SCREEN Holdings, SEMES, SFA Engineering, Shenzhen Liande, SNU Precision, TEL, TES, Top Engineering, Toptec, ULVAC, Vessel, Viatron Technologies, V-Technology, Wonik IPS, Wuhan Jingce and Y.A.C. Revenue for Q220 was $1.8b down 20% Y/Y, and up 6% sequentially. Q120 and Q220 were the lowest revenue quarters in years as panel makers cut down on capex. The top 5 display equipment suppliers were AMAT, SFA, ULVAC, TEL and V Technology. Of those companies, only AMAT, SFA and V Technology gained share. The top 5 accounted for 49% of the market, up from 45% last quarter.

Despite the overall reduced equipment sales in the quarter, 16 companies grew Y/Y, while 19 declined and operating income rose 22% Y/Y to the highest since Q1'19. Operating margins rose from 8.1% to 9.8%, also the highest since Q1'19. DSCC did not comment on the low revenue yet high operating income from the display equipment suppliers.

Figure 1: FPD Equipment Supplier Revenue

The display equipment market for Korean companies has been a hit or miss proposition recently, with those supplying equipment to Chinese panel producers seeing delays, while those producing tools for advanced products seeing strong sales. Recently listed Shindo ENG seeing a sales drop of 58% Y/Y, a result of COVID-19 delays at new OLED projects in China, while K-Mac, a producer of display inspection systems saw a slight decrease in sales but a 78% increase in backlog in 1H20, as it is the main supplier of tools that measure the thickness of deposited films, such as those used in OLED displays.

DSCC surveyed 35 display equipment companies including Applied Materials, AP Systems, Avaco, Canon (Tokki), Charm, Coherent, Contrel, Device ENG, DMS, EO Technics, Han's Laser, HB Technology, ICD, Invenia, Jusung, KC Tech, KMAC, LIS, Nikon, Nissin Electric, Philoptics, SCREEN Holdings, SEMES, SFA Engineering, Shenzhen Liande, SNU Precision, TEL, TES, Top Engineering, Toptec, ULVAC, Vessel, Viatron Technologies, V-Technology, Wonik IPS, Wuhan Jingce and Y.A.C. Revenue for Q220 was $1.8b down 20% Y/Y, and up 6% sequentially. Q120 and Q220 were the lowest revenue quarters in years as panel makers cut down on capex. The top 5 display equipment suppliers were AMAT, SFA, ULVAC, TEL and V Technology. Of those companies, only AMAT, SFA and V Technology gained share. The top 5 accounted for 49% of the market, up from 45% last quarter.

Despite the overall reduced equipment sales in the quarter, 16 companies grew Y/Y, while 19 declined and operating income rose 22% Y/Y to the highest since Q1'19. Operating margins rose from 8.1% to 9.8%, also the highest since Q1'19. DSCC did not comment on the low revenue yet high operating income from the display equipment suppliers.

Figure 1: FPD Equipment Supplier Revenue

Other results included:

- 24 companies managed to grow Q/Q, 1 was flat and 10 were down.

- Viatron, Device Eng., Philoptics, ICD, Nissin, Toptec, KMAC and EO Technics were all up over 100% Y/Y in display equipment revenues on OLED strength.

- Display equipment revenues rose from 9% to 10% of total revenues for these companies. If Canon is removed, display equipment was 14% of these companies’ revenues.

- Equipment company gross margins were flat at 39% with operating margins flat at 10%.

- Display equipment bookings fell 45% Q/Q and were down 16% Y/Y for 14 companies as COVID-19 made it difficult to meet with customers to close new orders.

- Display equipment backlog for 18 companies fell 5% Q/Q, but was up 30% Y/Y.