Vertical Divider

Chinese Report YTD Display Revenues thru September’20 Were US$82.723b, up 8.6% Y/Y

At the 2020 Chongqing Micro-LED Industry Innovation Forum and Konka Semiconductor Display Technology and Product Launch Conference held in China, Liang Xinqing LCD Branch Secretary of the China Optics and Optoelectronics Manufacturers Association disclosed that the global display device output value in the first three quarters of 2020 was US$82.723b, an increase of 8.6% Y/Y. The shipment area was 178m square meters, an increase of 5.7% Y/Y. For the first three quarters of 2020 in Mainland China TFT-LCD shipment area was 97.01m square meters, which accounts for 54.5% of the global market and the output value is $26.685b. In the first three quarters, the AMOLED shipment area was 1.09 million square meters, accounting for 0.6% of the global market, and the output value was US$2.709 billion. Liang Xinqing also mentioned domestic shortcomings. Currently, Japan has mastered the upstream core technology, South Korea’s OLED is the world leader and China had an advantage in LCD production capacity, but the technology structure is production oriented and the entire supply chain is dependent on non-Chinese sources.

Large Panel Display sales increased 2.3% sequentially and 41.7% Y/Y in November. Overall large panel shipments grew 67% however TV shipment growth declined for the 2nd month in a row, while November’s steep increase (+6.7%) in aggregate TV panel pricing offset the decline in units shipped last month and will likely do the same in December, given that TV panel prices are expected to rise 6.0% in December.

Panel producers are expected to continue raising TV panel prices, but some TV panel producers are concerned if price increases continue thru 1Q 2021, TV set makers will no longer be able to absorb the margin hit and will start raising set prices, which could reduce demand. On a 3 year and 5-year basis, January TV panel pricing has declined 1.3% and 5.9%, but in 2017 there was a very steep decline in January (-23.5%) that had a significant effect on the 5-year average.

TV set brands have borne the brunt of these panel price increases, especially as they roll through older, lower cost inventory. While there was discounting during the recent holidays, it will be progressively harder to offer similar discounts going forward without further margin erosion. There is some margin ‘sharing’ with retailers, but TV set brands must also consider the elasticity of TV set product and with slower demand months ahead. The objective for both panel producers and TV set brands was to move as much product as possible before the end of the year and into Chinese New Year, so concerns about 2021 demand are secondary considerations at the moment.

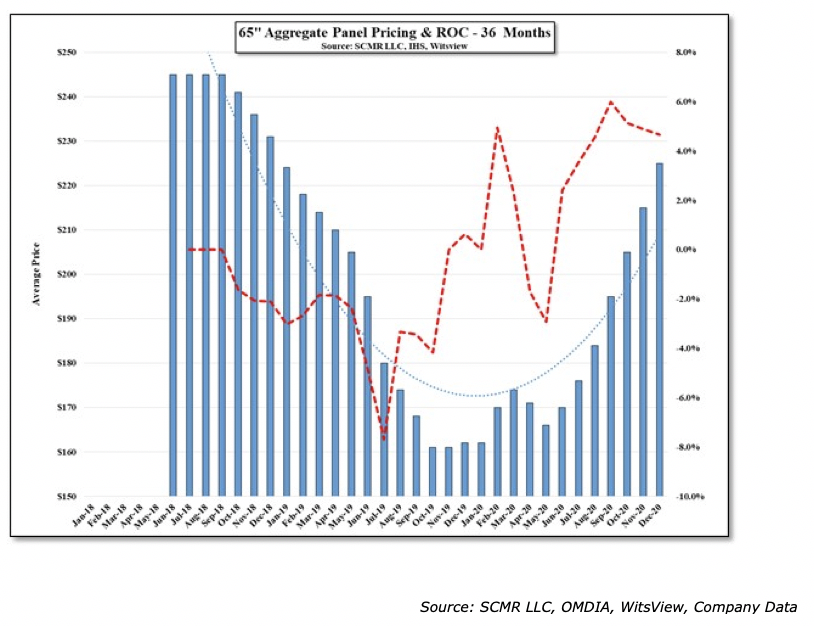

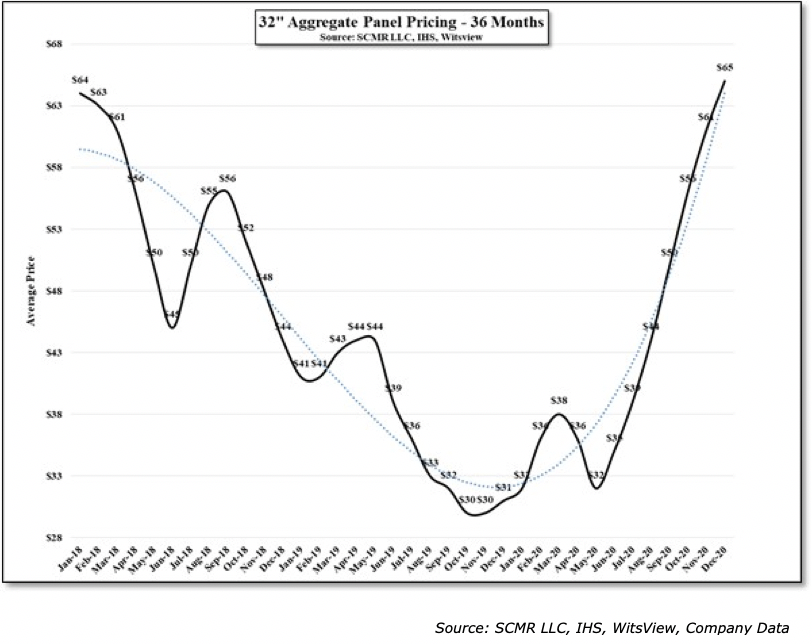

Looking at 32” TV panel pricing on a 3-year basis, the aggregate price of 32” TV panels is now 1.6% higher than it was in January 2018, 58.5% higher than it was in January 2019 and 103% higher than it was in January of this year. 65” TV panel pricing, which has a much shorter pricing history, still remains 8.2% below peak, but is 52.2% above its low in October of 2019.

Figure 1: 32" Aggregate Panel Pricing - 36 Months

At the 2020 Chongqing Micro-LED Industry Innovation Forum and Konka Semiconductor Display Technology and Product Launch Conference held in China, Liang Xinqing LCD Branch Secretary of the China Optics and Optoelectronics Manufacturers Association disclosed that the global display device output value in the first three quarters of 2020 was US$82.723b, an increase of 8.6% Y/Y. The shipment area was 178m square meters, an increase of 5.7% Y/Y. For the first three quarters of 2020 in Mainland China TFT-LCD shipment area was 97.01m square meters, which accounts for 54.5% of the global market and the output value is $26.685b. In the first three quarters, the AMOLED shipment area was 1.09 million square meters, accounting for 0.6% of the global market, and the output value was US$2.709 billion. Liang Xinqing also mentioned domestic shortcomings. Currently, Japan has mastered the upstream core technology, South Korea’s OLED is the world leader and China had an advantage in LCD production capacity, but the technology structure is production oriented and the entire supply chain is dependent on non-Chinese sources.

Large Panel Display sales increased 2.3% sequentially and 41.7% Y/Y in November. Overall large panel shipments grew 67% however TV shipment growth declined for the 2nd month in a row, while November’s steep increase (+6.7%) in aggregate TV panel pricing offset the decline in units shipped last month and will likely do the same in December, given that TV panel prices are expected to rise 6.0% in December.

Panel producers are expected to continue raising TV panel prices, but some TV panel producers are concerned if price increases continue thru 1Q 2021, TV set makers will no longer be able to absorb the margin hit and will start raising set prices, which could reduce demand. On a 3 year and 5-year basis, January TV panel pricing has declined 1.3% and 5.9%, but in 2017 there was a very steep decline in January (-23.5%) that had a significant effect on the 5-year average.

TV set brands have borne the brunt of these panel price increases, especially as they roll through older, lower cost inventory. While there was discounting during the recent holidays, it will be progressively harder to offer similar discounts going forward without further margin erosion. There is some margin ‘sharing’ with retailers, but TV set brands must also consider the elasticity of TV set product and with slower demand months ahead. The objective for both panel producers and TV set brands was to move as much product as possible before the end of the year and into Chinese New Year, so concerns about 2021 demand are secondary considerations at the moment.

Looking at 32” TV panel pricing on a 3-year basis, the aggregate price of 32” TV panels is now 1.6% higher than it was in January 2018, 58.5% higher than it was in January 2019 and 103% higher than it was in January of this year. 65” TV panel pricing, which has a much shorter pricing history, still remains 8.2% below peak, but is 52.2% above its low in October of 2019.

Figure 1: 32" Aggregate Panel Pricing - 36 Months

Figure 2: 65" Aggregate TV Panel Pricing & ROC - 30 Months