Vertical Divider

Another Month Another Leader of China’s Smartphone Industry

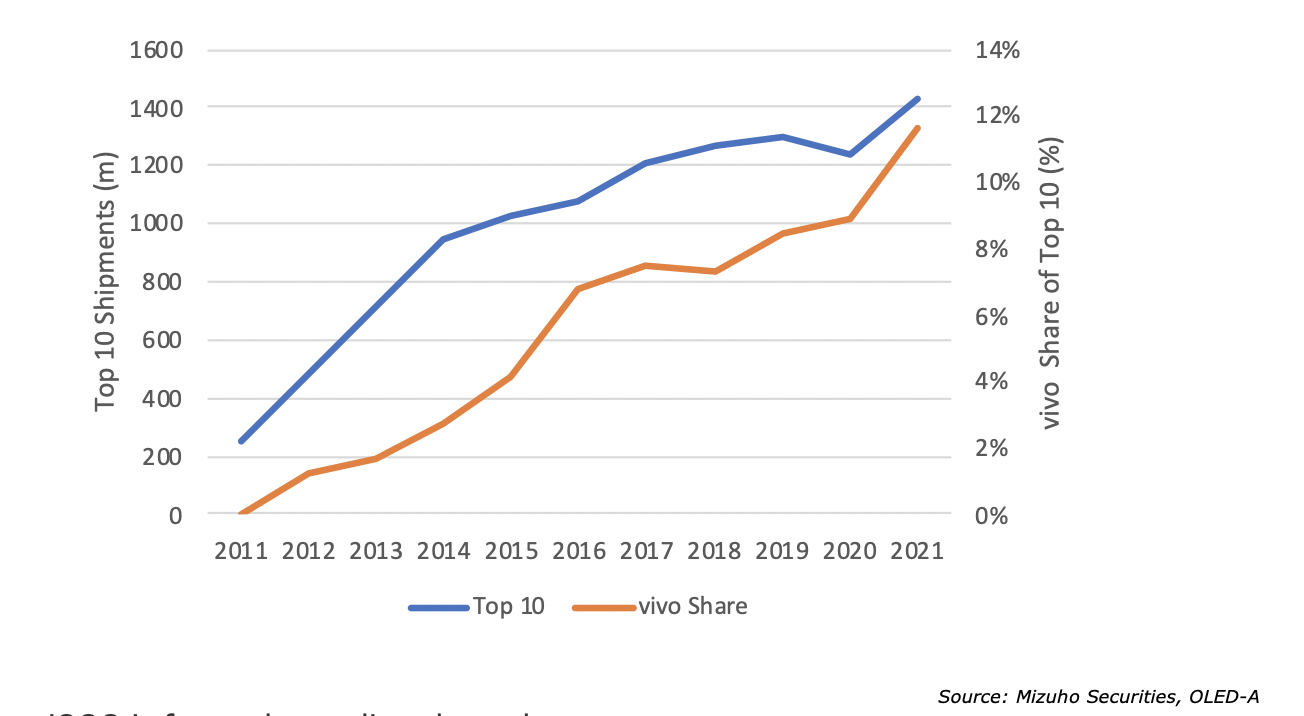

Vivo has overtaken OPPO to emerge as the top smartphone vendor in the China market in week 11 (March 8-14) of 2021, riding on the strong performance of its budget model Y3 and S9, according to according to Counterpoint’s China Smartphone Weekly Tracker. Vivo (including iQOO) was again able to jump ahead of OPPO (excluding Realme and OnePlus) in week 13 to hold a market share of 24% while Oppo garnered a 21% share. Huawei (excluding Honor) stood at a distant third position with a market share of 15% in week 13 as it continues to battle with U.S. sanctions and now chip shortage. Vivo was one of the first brands in the market to launch 5G devices, with the Nex 3 5G and iQOO Pro 5G in August 2019 and September 2019, respectively. Its 5G portfolio has seen strong sales too, accounting for more than 76% of its sales in February, up from a meagre 0.5% in August 2019.

Currently, vivo’s portfolio includes the NEX, X, S, Y series, and sub-brand iQOO. The NEX and X series are vivo’s flagship series focused on camera capabilities while the S and U series are focused towards customers seeking value for money smartphones.

Figure 1: Vivo Market Share vs. Top 10 Volume

Vivo has overtaken OPPO to emerge as the top smartphone vendor in the China market in week 11 (March 8-14) of 2021, riding on the strong performance of its budget model Y3 and S9, according to according to Counterpoint’s China Smartphone Weekly Tracker. Vivo (including iQOO) was again able to jump ahead of OPPO (excluding Realme and OnePlus) in week 13 to hold a market share of 24% while Oppo garnered a 21% share. Huawei (excluding Honor) stood at a distant third position with a market share of 15% in week 13 as it continues to battle with U.S. sanctions and now chip shortage. Vivo was one of the first brands in the market to launch 5G devices, with the Nex 3 5G and iQOO Pro 5G in August 2019 and September 2019, respectively. Its 5G portfolio has seen strong sales too, accounting for more than 76% of its sales in February, up from a meagre 0.5% in August 2019.

Currently, vivo’s portfolio includes the NEX, X, S, Y series, and sub-brand iQOO. The NEX and X series are vivo’s flagship series focused on camera capabilities while the S and U series are focused towards customers seeking value for money smartphones.

Figure 1: Vivo Market Share vs. Top 10 Volume

iQOO is focused on online channels.

Figure 2: China’s Weekly Market Share

Figure 2: China’s Weekly Market Share

Xiaomi witnessed the sharpest shipment growth of 126% on-year and posted strong sales numbers in Egypt, Morocco, Nigeria, and Kenya. It is expected to see market gains in 2021.

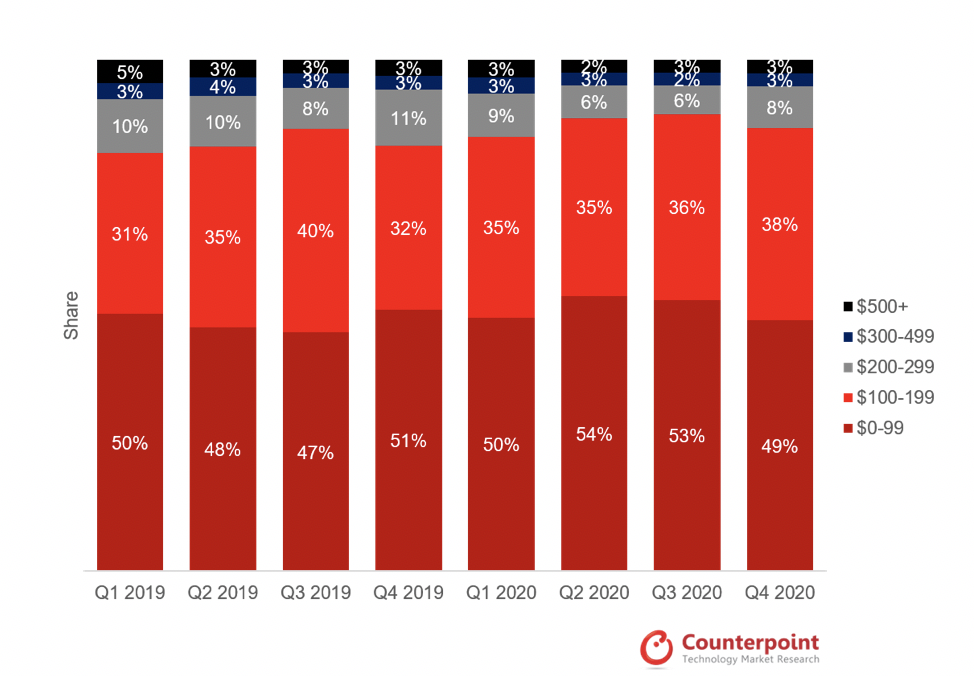

OPPO’s shipments grew 57% on-year and it is likely to make a strong push in the high mid-price segment. The ASP decreased 15% between 2018 and 2020, with the sub-$200 segment accounting for over 80% of Africa’s smartphone sales. Further replacement of feature phones by entry-level smartphones will keep the ASP under pressure in the next few years.

Figure 3: China’s Smartphone Share by ASP

OPPO’s shipments grew 57% on-year and it is likely to make a strong push in the high mid-price segment. The ASP decreased 15% between 2018 and 2020, with the sub-$200 segment accounting for over 80% of Africa’s smartphone sales. Further replacement of feature phones by entry-level smartphones will keep the ASP under pressure in the next few years.

Figure 3: China’s Smartphone Share by ASP