Vertical Divider

5G Devices in 2020 Focused on Sub6 Service

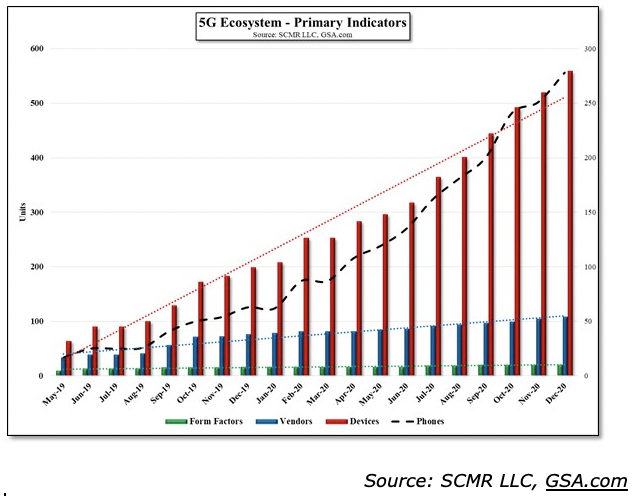

2020 was really the first year of meaningful 5G sales, as only 63 5G smartphones were offered or announced in 2019 (24 were not released until 2020). The number of 5G devices grew 180.9% Y/Y encompassing 20 form factors, with 5G smartphone offerings as part of that device count growing 341.3% Y/Y. Sub6, was by far the most popular band as the cost of providing coverage to carriers is considerably lower than that of mmWave, regardless of the fact that speed and bandwidth are lower for sub6. Sub6 devices grew 275.2% y/y while mmWave grew 71.2%, while those devices that were able to provide both bands grew 38.8%. As the cost of modems declines, we expect devices with dual band coverage to increase more rapidly.

5G globally is in the early stages of roll-out and much of the potential bandwidth has yet to be allocated in many countries. The following tables provide info on auctions, assignments, and trials are in a number of countries, although there is considerable nuance to each category and country. There are ‘bands within bands’ that can make a difference to performance, and in many countries there are still many conflicts over potential assignments, so much will change over time.

Figure 1: 5G Ecosystem - Primary Indicators

2020 was really the first year of meaningful 5G sales, as only 63 5G smartphones were offered or announced in 2019 (24 were not released until 2020). The number of 5G devices grew 180.9% Y/Y encompassing 20 form factors, with 5G smartphone offerings as part of that device count growing 341.3% Y/Y. Sub6, was by far the most popular band as the cost of providing coverage to carriers is considerably lower than that of mmWave, regardless of the fact that speed and bandwidth are lower for sub6. Sub6 devices grew 275.2% y/y while mmWave grew 71.2%, while those devices that were able to provide both bands grew 38.8%. As the cost of modems declines, we expect devices with dual band coverage to increase more rapidly.

5G globally is in the early stages of roll-out and much of the potential bandwidth has yet to be allocated in many countries. The following tables provide info on auctions, assignments, and trials are in a number of countries, although there is considerable nuance to each category and country. There are ‘bands within bands’ that can make a difference to performance, and in many countries there are still many conflicts over potential assignments, so much will change over time.

Figure 1: 5G Ecosystem - Primary Indicators

Figure 2: 5G Frequency Band Device Share